The growth of private debt in Europe has its origins in the Global Financial Crisis

Brian Kane, Director of Capital Markets and Origination at CrossLend, spent the best part of seventeen years working at a ratings agency in Europe from 1997 to 2015. There he had a ringside seat to the emergence of a range of new funding instruments and asset classes in the public securitisation markets.This reached its peak in the decade leading up to the Global Financial Crisis (GFC). Everything changed after 2008, when the ensuing scrutiny by regulators in Europe tamped down the market. Kane believes that the restrictive regulations that were put in place following the GFC have served to push more activities into the private debt space.

Brian, you worked at Standard & Poors [now S&P Global Ratings] for seventeen years, including during the GFC. What were some of the major market trends you saw develop during that time?

Brian Kane: I joined Standard and Poor’s in 1997 and developed professionally alongside the growth of the European securitisation markets. I worked as an analyst on many first time asset class issuances in Europe’s public securitisation markets, including German mortgage transactions, covered bonds, shipping transactions, CMBS, and aircraft deals across many jurisdictions. These were obviously rated and broadly syndicated deals.

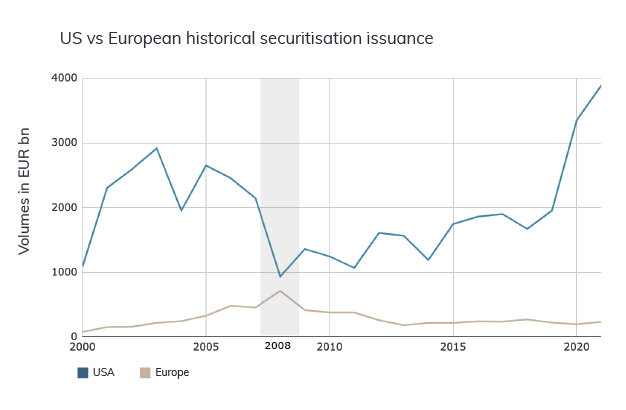

Spurred on by the growth and wider application of structured finance as a funding tool in the much larger US market, the European market grew from strength to strength. From its early beginnings in the late 1990s, by 2006 public securitisation issuance volumes had reached nearly 500bn euros annually, with its apogee in 2007 when securitisations worth over 700bn euros were issued, according to figures published by the Association for Financial Markets in Europe (AFME). Across Europe, real economy asset classes that had traditionally been funded by banks – especially consumer, SME loans, buy to let mortgages, leasing assets, auto, and whole business assets – were now being originated in a systematic fashion and offered to global investors on a tranched or risk return basis.

Distinct asset classes developed and grew, with different levels of credit risk and liquidity. This allowed investors from across the globe to build diversified portfolios of transactions backed by cash flows from diverse asset types. Investors had to develop strong credit skills to understand the performance and relative value of the underlying assets that were being funded. This was important because it was the performance of the underlying assets that determined the returns they would see.

But after the 2008 global financial crisis, as I saw it, the brakes were largely slammed shut on any kind of innovation within the European public asset backed security (ABS) market. There was a lot of scrutiny from regulators surrounding securitisation as a funding tool. While some will say that this was warranted given the circumstances, volumes have never quite recovered in Europe as a result.

That said, since then the European public securitisation market has largely been a well-functioning market. The major issue is that operating within it has become highly complex both for originators and investors due to the sheer weight of regulation imposed on market participants. Originators must comply with a variety of regulations as well as different templates and reporting schedules.

Equally, the necessity for ABS investors to adhere to numerous regulations has, to some extent, reduced the attractiveness of public ABS securities, in comparison to say, corporate bonds or investing in direct lending or other types of private credit funds.

One outcome has been growth in collateralised loan obligations (CLOs) as a greater proportion of total issuance. Here we are largely talking about leveraged loans. For example, in 2014, CDOs and CLOs made up around 6.5% of total issuance; by 2021, they made up around 18.5% of total issuance. But interestingly enough, not all the regulations apply to CLO transactions (notably the simple transparent securitisation [STS] regime); which apply to things like mortgage transactions, consumer loans and auto financing. My perception is that in the broader industry, there is a lot of frustration around how regulation has generally evolved.

It’s interesting – subprime mortgage securitisations in the United States are seen as a major driver of the Global Financial Crisis, yet data shows that public securitisation issuance volumes in the US quickly recovered after ’08, whereas issuance volumes in Europe stagnated.

So the irony of all this is while it was problems emanating from the US subprime market that led to the global contagion – the epicentre of the crisis – that particular jurisdiction has been able to bounce back a lot quicker.

In my view, that is largely because in the US, they have a much more progressive attitude towards financial crises. US capital markets are much deeper than those in Europe, they are understood to be important engines driving overall economic growth, and the approach there seems to be to quickly identify the problem and develop a remedy or a solution. Regulators there are also a lot closer to the functioning of the markets.

As I see it, the European public securitisation markets have faced comparatively more restrictions than the US since 2009, even though the market failures were centred in the US. When you look at it, the credit performance of the European securitisation market for assets written prior to 2007 was actually very good. There were very few actual credit losses in public securitisations. There were, of course, market value losses where a lot of investors were forced to sell assets at low prices, but ultimately, most of those assets returned to par.

So what did you see in the years after 2008?

Post GFC, I was heading up the commercial side of structured finance ratings at S&P, after previously running the residential mortgage-backed securities (RMBS) business in Europe. During the whole post-crisis period, I saw how investors were approaching the opportunities available.

A lot of credit opportunity funds were launched in 2008 through to 2013. These were typically large US credit funds, and their initial focus was the “pull to par trade”, where they bought discounted asset backed securities that were money-good, had high ratings, but where there wasn’t enough liquidity. So that was the first wave of money that came in.

That trade went away as those securities returned to par. And then those funds started buying actual portfolios, because at this time, the banking system was deleveraging and banks were looking to take assets off their balance sheets. So a number of these credit funds began bidding on portfolios. Once the portfolios were repaired, they then needed to be exited, or refinanced and sold on. This trade is still ongoing in some markets, like Italy and Spain, where there are active NPL markets.

What credit funds then started to do was to actually buy platforms, meaning they could originate assets directly. Private equity credit funds started to buy large ticket portfolios, such as four or five billion sterling in UK mortgages. They were buying them and simultaneously executing securitisation strategies, essentially leveraging a 5% retained equity piece.

Real estate was another area where you saw innovation by funds. Especially on high value marquee assets with stable long term tenants and returns – the owners would be looking for loans in the hundreds of millions of euros, which banks weren’t in a position to lend on. Insurance companies started to issue private debt property funds focused on commercial real estate – mainly senior CRE funds – and they benchmarked these against corporate investment grade credits.

So you saw this big growth in private debt and alternative credit after 2008?

While public securitisation markets have been diminished by the impact of regulation, the private securitisation markets in Europe, and even globally, are massive. It’s like an iceberg – the public markets are what you see above water. Below the water is the private bilateral securitisation market, which is multiples in size of public markets.

The effect of regulation was that people created a workaround. The reality is that those assets were still getting funded, but not by asset-backed commercial paper – they’re not getting funded in publicly rated, AAA to BBB deals. Instead, capital is being raised in a fund or a private securitisation format. So what we saw was the recharacterisation of securitisation, away from public instruments, and the subsequent growth of private debt and private credit post the financial crisis.

Of course in parallel we also saw the banks deleveraging, with reduced ability to fund typical corporate loans. There’s a lot of focus on the impact on SMEs, meaning smaller companies, and micro-enterprises, but also in the mid-sized corporate loans space, banks are not able to adequately service these because of the risk weightings. So direct lending investors in the private markets have stepped in to fund all kinds of corporate credit.

Again, as I see it there is a clear split between the US and Europe: whereas in the United States investors were quick to embrace the possibilities in private debt and credit, in Europe, it’s been a slow, painful turn. Nevertheless, in the past few years, given the scarcity of positive yielding assets and interest in private debt, we have seen a growing interest in strategic lending partnerships.

This development of private debt as an attractive asset class for investors came during the period of historically low interest rate benchmarks where we saw unprecedented growth in negative yielding assets.

What came next for you?

I left S&P in 2015, and later became head of capital markets of a UK-based non-bank financial company. While there, I was active in raising a significant volume of funds via warehousing and forward flow funding. Forward flow was and is a popular way to raise funds – it’s especially effective when you have a bank which has a low cost of funds and they’re matched with a non-bank originator such as a digital lender who is originating assets at a relatively high rate of return, but they don’t have a broad funding base.

Then you joined CrossLend in 2018. What attracted you to this company?

After that experience I wanted to be in a position to help financial technology companies – FinTechs – get institutional funding. I wanted to take all of my accumulated expertise in structured finance, securitisation, and legal structuring, as well as knowledge about investors’ appetite and risk returns, and put it directly into a FinTech company, to help them. I had followed developments in the US where originators like Lending Club, SoFi and Upgrade were using technology to automatically underwrite assets and to fund them, and it was clearly an attractive model.

Initially what attracted me to CrossLend was the high tech, even scientific approach to securitisation, data, and the private debt space in general. We have a lot of expertise in data science and in coding which is reflected in the development of our platform. Technology is the great equaliser.

What is the market opportunity? In part, people still largely underestimate how inefficient legacy banks are, and also how resistant to change the management in those banks are. So there’s a whole confluence of factors that basically leads to quite an inefficient and even inept funding system. There will be a lot of disruption and in my view, the often quoted reference that the “digitisation of banks is not even 1% done” is certainly correct.

So how do you see the potential impact of CrossLend in terms of the real economy?

CrossLend is enabling bank and non-bank originators to tap the debt capital markets by providing them with the infrastructure that enables private debt and private credit investors to access, source, understand, analyse, and deploy capital in bilateral private debt deals. And we can do this in a very disruptive, efficient way.

Ultimately, CrossLend aims to make the overall debt ecosystem more efficient, ultimately to reduce the funding costs to end users. For example, that can mean reducing the borrowing costs for SMEs by bringing cheaper, more diversified funding into the market, which can have flow-on effects for the general economy such as increased employment or enabling entrepreneurship.

Any views expressed in this interview are the personal views of the interviewee, and do not necessarily reflect the position of CrossLend or its employees. This article should not be construed as investment advice, or relied upon by anyone as legal, accounting, compliance or tax advice, or for any other purposes. This article is not to be construed, under any circumstances, by implication or otherwise, as an offer to sell, nor as a solicitation to buy securities.

Related articles

Securitisation: active management option to boost Luxembourg hub

The overhaul of Luxembourg’s securitisation laws introduced a number of changes, notably allowing for active management and a broader [...]

Originator Spotlight/Lenderwize

A fast-growing trade finance platform, Lenderwize specialises in invoice financing in the digital economy. Currently its platform provides its [...]

Digital lending emerges as an important sub-segment of private debt

Amid increasing breadth within the private debt asset class, specialised investors can allocate capital to sub segments in a bid [...]